Meridian Home Mortgage is a non-bank lender offering conventional, VA, FHA and jumbo loans as well as refinances. This Westminster, Maryland mortgage lender was founded in 2001 and has grown to over 100 employees providing mortgages in 44 states and the District of Columbia. The company boasts no upfront costs, such as a good faith deposit, a straightforward approach and teams that don’t work on commission.

Today's Rates

| Product | Today | Last Week | Change |

|---|---|---|---|

| 30 year fixed | 5.75% | 5.88% | -0.13 |

| 15 year fixed | 5.25% | 5.44% | -0.19 |

| 5/1 ARM | 6.06% | 6.06% | 0.00 |

| 30 yr fixed mtg refi | 7.21% | 7.13% | +0.08 |

| 15 yr fixed mtg refi | 6.59% | 6.73% | -0.14 |

| 7/1 ARM refi | 6.13% | 6.13% | 0.00 |

| 15 yr jumbo fixed mtg refi | 3.06% | 3.10% | -0.04 |

National Mortgage Rates

Regions Served by Meridian Home Mortgage

Does Meridian Home Mortgage Operate in My Area?

Meridian arranges mortgages in 49 states and the District of Columbia. The only state that they are not currently servicing is Hawaii.

What Kind of Mortgage Can I Get With Meridian Home Mortgage?

Conventional: The standard mortgage loan is a conventional loan. You can choose a fixed-rate loan or an adjustable-rate mortgage (ARM). Like the name suggests, the interest rate stays “fixed” for the life of a fixed-rate loan, ensuring your mortgage payments (principal and interest) stay the same month after month. Most homebuyers choose fixed-rate loans. Meridian Home offers fixed-rate loans from 10 to 30 years in increments of five.

The interest rate on an adjustable-rate mortgage is generally lower than with a fixed-rate loan for an initial period, once that period ends, the rate can change generally once a year and will usually go up. ARMs are offered in 3/1, 5/1, 7/1 and 10/1 terms. The first number indicates the number of years your interest rate stays fixed and the second number indicates how many times per year your interest rate adjusts after the initial term expires. For example, a 5/1 ARM will have the same interest rate for five years, and then once a year after that, your interest rate will increase or, less likely, decrease.

Jumbo loan: When the home you’re purchasing costs more than conventional loan limits, you’re required to get a jumbo loan. The national loan limits range from $726,200 to $1,089,300, depending on where you live in 2023. But the "floor" limit for a single-family loan could be as low as $472,030.

VA loan: The Department of Veterans Affairs backs this loan aimed at service members, veterans and eligible National Guard and Reserve personnel as well as select spouses. This borrower-friendly loan has no down payment requirement and no private mortgage insurance.

FHA loan: This Federal Housing Administration-backed loan helps those with low credit scores and low down payment savings achieve homeownership. You can put as little as 3.5% down and the funds can come from gifts or grants. FHA loans come with a version of mortgage insurance, which is an additional cost on top of your monthly payments.

Refinance: Meridian Home Mortgage offers VA streamline loans (IRRRL), FHA streamline loans and conventional refinancing options with fixed-rate or ARM terms.

What Can You Do Online With Meridian?

Light on substance, heavy on well-crafted design, Meridian’s website delivers the least amount of information in the most clear way. You can find contact information, reviews and loan options, but you won’t find many specific details. For example, under the “our loan programs” heading, loan types are listed, such as conventional loan, VA loan and FHA loan, but there’s no further information. Even though the loan types are in boxes, the tiles are unclickable. You get the name but not the description or any information about requirements, such as credit score or income.

Everything on the site points you to the “get started” button which leads you to a prequalification form, complete with an optional input for your Social Security number to pull your credit. There are no calculators, such as the common one found on mortgage sites that helps you find out how much house you can afford. There isn’t a blog or article database or a frequently asked questions section, there’s no available rates listed and there aren’t any videos or alternate content guides. You won’t find a homebuyers education course or any first-time homebuyer content.

In summary, the most you can do with the site is submit your prequalification (which is really closer to a contact form) or find the company’s phone number to get in contact with a loan officer directly.

Would You Qualify for a Mortgage From Meridian?

Your credit score is the first financial marker most lenders check. It provides a snapshot of your credit and lending history, giving the lender an idea of how much risk you would be as a borrower. In general, Meridian has a FICO score minimum of 560. That’s pretty generous given that many lenders start at 620 or higher. That said, your credit score isn’t the only consideration for qualification. You won’t get the best rates or terms with a credit score that low. Ideal rates and terms are offered when you’re in the 740 or higher range.

Another important financial marker is your income and your debt. These two figures help the bank understand how much money you have available each month to pay your mortgage as well as all your other debt. This is generally expressed as a percentage known as the debt-to-income (DTI) ratio. To calculate your DTI, add your monthly debt payments, including car loans, student loans, alimony, child support, credit card payments and your potential new monthly mortgage payment. Divide that figure by your monthly pre-tax income and multiply by 100. That’s your DTI. Most lenders have a rough maximum DTI, such as 41%. You generally want to be in the 36% or below range to have a chance at the best rates and terms.

Down payment savings is the next consideration. If you’re applying for a conventional loan, 20% is the ideal amount. You won’t have to pay private mortgage insurance with 20% down, and you’ll have that much equity in your home to start. That said, FHA and VA loans don’t require significant down payment savings, in fact, VA loans allow 0% down. Although you may not need to demonstrate down payment savings, you will still need savings to pay for closing costs. You’ll want to keep that in mind when you apply for a loan, closing costs can add up to thousands of dollars and can be a burden if you haven’t planned ahead.

What’s the Process for Getting a Mortgage With Meridian?

Meridian’s loan process is clearly spelled out on its website. Below is a recap of the five steps to apply for a loan with the company.

Step 1: Fill out a quick form.

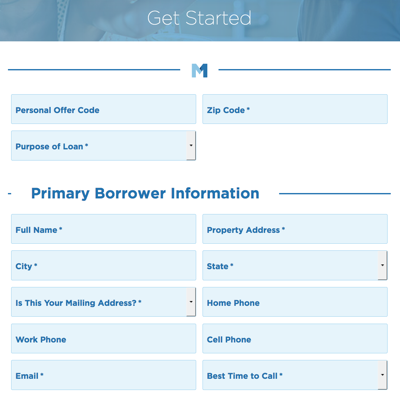

The “get started” form asks contact information, loan term, goal, financial information including your current employer, position, income, savings and retirement amount, property information, Social Security number and co-borrower information, if applicable. Once you finish this step, a Meridian loan officer will contact you and give you rates, terms and possibly payments.

Step 2: Submit documents.

In general, you’re required to provide tax returns, W-2s, pay stubs, bank account statements, Certificate of Eligibility for VA loans, asset information and any other relevant financial documentation.

Step 3: Appraise home.

Meridian will schedule and for an appraisal of the home you plan to buy. If it’s a refinance, Meridian will pay the appraisal fee. For purchase loans, this cost is usually paid for during closing.

Step 4: Lock in your rate.

Your loan is finalized and submitted to underwriting, which is the second-to-last step.

Step 5: Close your loan.

The final step is when you sign the paperwork and the loan is funded. This generally happens on the day you close and get the keys to your new home.

How Meridian Home Mortgage Stacks Up

In terms of availability, Meridian Home Mortgage is in 40 states, which is more than many small lenders. However, while the company originates loans in those locations, there are no in-person offices, which puts it on par with a lender such as Quicken Loans or Ally. But, Meridian doesn’t offer the online capabilities and availability Quicken offers, or the retail banking options that Ally offers. The prequalification form doesn’t yield any answers after you submit, instead you land on a page with the promise of a phone call from a Meridian Home Mortgage representative. There are no interactive tools or widgets and you can’t find any rate offers.

That means it’s hard to say why you should choose Meridian Home Mortgage over all the other banks out there. However, the company expects that thought and counters with a section titled “What Makes Meridian Different,” which includes no upfront costs (good faith deposits aren’t required) and agents that don’t work on commission, promising a pressure-free environment.

The company had minimal wait time when SmartAsset called to find out about loan options, and friendly, informative representatives. The website is clear, although, as we previously mentioned, it contains minimal information. You’ll likely interact on the phone for the majority of your relationship with Meridian, which is fine unless you prefer a mostly digital experience. If that’s more in tune with what you’re looking for, Rocket Mortgage, Better Mortgage or Lenda are all good options.

However, if you’d like to complete your mortgage in person, or prefer to keep your mortgage in the same spot as your retail banking, Chase, Wells Fargo or Bank of America may make more sense as your mortgage lender.

Tips for Finding a Mortgage

- There can seem to be an endless sea of loan options when you're mortgage hunting, but there is one thing to look for if you find two similar lenders. While interest rates are flat, annual percentage rates (APRs) include outside charges, like closing costs and other fees. So if one lender has a larger difference between their interest rates and APRs than another, you may want to choose the one with presumably lower fees.

- A financial advisor can help you choose a mortgage that fits into your financial plan. SmartAsset free tool matches you with up to three vetted financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.